Welcome back to Lambergg’s Insiders.

If you look around the internet right now, you will see a massive wave of "trust educators," TikTok influencers, and family attorneys all selling the exact same dream: “Just open a Revocable Living Trust, put your house and bank accounts into it, and you are completely protected from the outside world.”

It sounds clean. It sounds easy.

But today, we need to have a very raw, honest conversation about why relying on this specific structure is the most dangerous estate planning mistake you can make.

If your current estate planning binder contains a standard "Grantor Trust" where you hold all the keys, you have a ticking time bomb on your shelf. When a real lawsuit hits or a creditor comes knocking, a sharp attorney will rip that document to shreds in less than 60 seconds.

Let's expose exactly why.

LEGACY TIP OF THE WEEK

Corporate Trustee

When people realize they shouldn't name themselves or a financially reckless relative as the independent trustee, they often look to big banks or corporate trust companies to manage their estate.

Corporate trustees charge an annual asset management fee, often between 1% and 2% of the entire trust estate every single year, whether the market goes up or down. On a $1.5 million estate, that is $15,000 to $30,000 drained out of your children’s inheritance every year just for administrative paperwork.

You do not need to pay Wall Street to protect your legacy. Inside a properly structured framework, you can name a trusted family friend or a professional CPA as a co-trustee, paired with a specialized "Trust Protector" clause. This allows your family to fire the trustee instantly if they overcharge, keeping the control, and the cash, entirely in your family's bloodline.

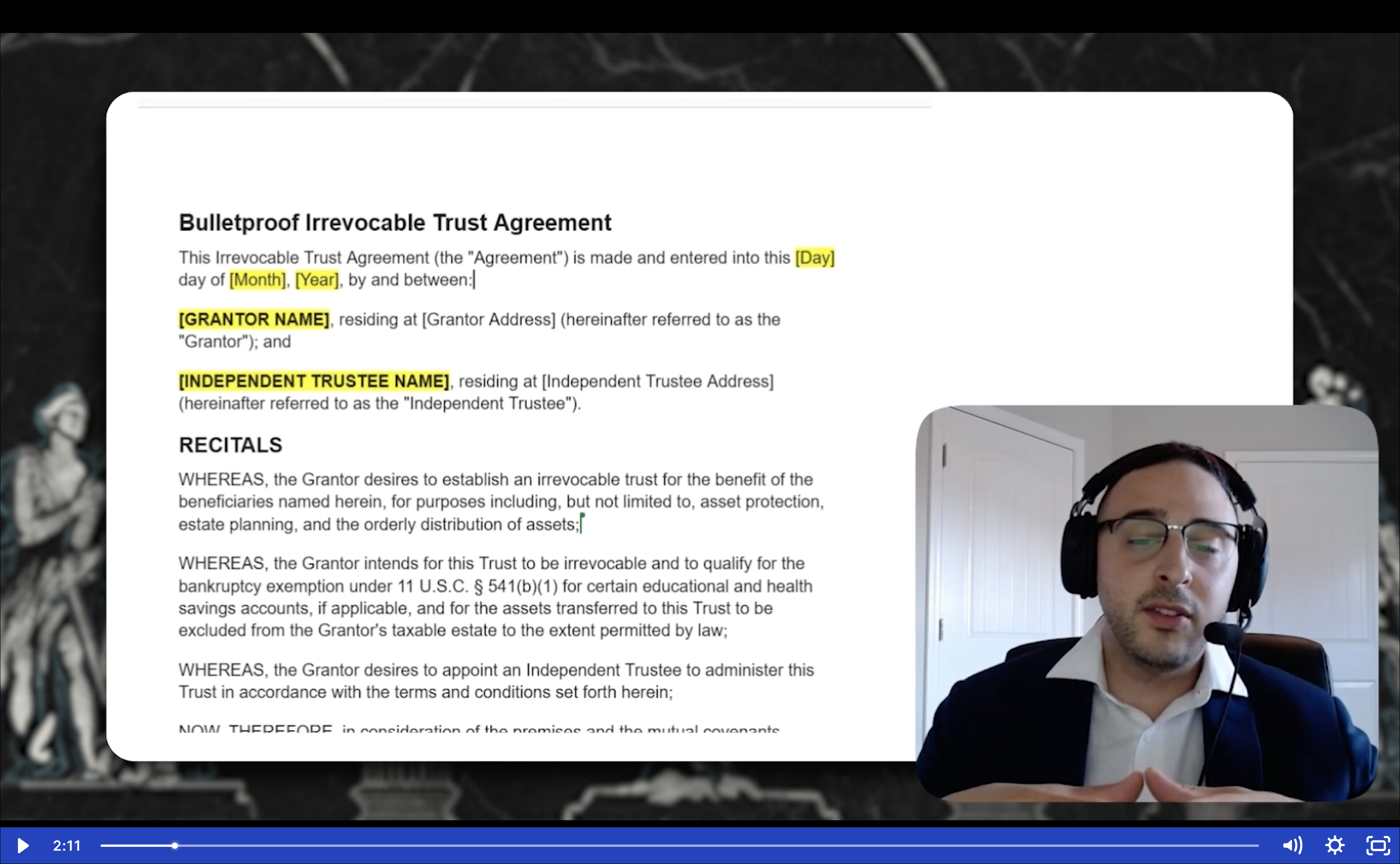

Why Your Living Trust is an "Alter-Ego"

In the legal system, there is a fundamental rule that governs asset protection: There must be a trust for there to be a trust. For a court of law to recognize a trust as an independent, impenetrable vault, the person who created it (the Grantor) must legally relinquish some level of control over what they put inside it.

Here is the mechanical breakdown of the classic Revocable Living Trust trap:

-

In a standard Revocable Living Trust or Grantor Trust, you wear three hats simultaneously. You are the Grantor (you created it), the Trustee (you manage the money day-to-day), and the Beneficiary (you spend the money on yourself).

-

Because you can change the trust, dissolve the trust, move money in and out of the trust, and spend it on your own dinner whenever you want, you have never actually relinquished control.

-

The moment a creditor sues you and takes you to court, a judge will look at your Revocable Trust and apply the "Control Test." The judge will state: "Since you have the absolute power to pull the money out of the trust and pay for your personal lifestyle, I am ordering you to pull that money out right now and hand it to the creditor." Legally, the court views a standard Revocable Grantor Trust as nothing more than a "DBA" (Doing Business As) or an alter-ego of you. It avoids probate when you die, yes - but it offers exactly zero protection from lawsuits, medical bills, or divorces while you are alive.

If a company or a lawyer tells you that you can act as the sole Grantor, sole Trustee, and sole Beneficiary while getting absolute lawsuit protection, steer clear. It is a legal impossibility.

To achieve true, ironclad asset protection, you must step across the line into an Irrevocable Asset Protection Trust structure. By utilizing independent trustees, co-beneficiary bloodlines, or specialized distribution clauses, you legally pass the "control test." You strip the judges and creditors of their power to pierce your vault, while still maintaining full operational enjoyment of your wealth.

CASE STUDY

The "Bulletproof" Document That Pierced Instantly

David (58) owned a successful regional consulting business. To protect his personal wealth, he paid a local firm $5,000 to draft a "Revocable Living Trust." He transferred his $600,000 primary home and his $300,000 non-retirement brokerage account into the name of the trust. He was listed as the Grantor, Trustee, and Lifetime Beneficiary.

David's business was hit with an unexpected breach-of-contract lawsuit from a disgruntled former corporate client. Because of a loophole in his commercial liability insurance, the policy refused to cover the claim. The opposing counsel won a personal judgment against David for $750,000.

(Anonymized from a recent asset-seizure ruling)

David smiled in the deposition, completely confident. He told the plaintiff's attorney, "Go ahead and try to collect. My house and investments are locked away inside a family trust."

The plaintiff's attorney didn't even flinch. They simply filed a motion to pierce the trust. In front of the judge, the attorney proved that David had complete, unfettered access to the trust assets, pointing out that David had used the trust bank account to pay for a personal family vacation just three months prior.

The judge immediately ruled that the trust was David's "alter-ego." The court order bypassed the trust entirely, liquidated David’s brokerage account, put a judicial lien on his home, and completely shattered his financial security. David learned the hard way that a trust without a restriction on control is just an expensive piece of paper.

The Exact Video Training Our Private Clients Use

If you want to ensure that your home, your business, and your cash stay exactly where they belong regardless of what happens with the global economy, you have to take the wheel.

The system wasn't built to protect you. It was built to move your money somewhere else.

We took our complete Bulletproof Trust private client training, the exact step-by-step program we charge up to $20,000 to build for high-net-worth families and recorded the entire thing on video.

Inside the Bulletproof Trust Secrets video training, our lead trust attorney opens the legal documents and walks you through them page by page. Line by line. You will learn exactly how to structure every clause and fund every asset to shield your legacy from lawsuits, probate, divorce, and the IRS.

You hit play. You pause. You follow along. You build your own fortress.

You will know more about trusts than 95% of general-practice attorneys. You will be in control. Not your lawyer. Not the government. You.

→ Click Here to Access the Video Training ←

Control and Identity

Do not wait for a process server to expose the structural flaws in your estate plan. Take 5 minutes to audit your trust setup today:

-

[ ] The Hat Trick Check: Pull your trust agreement. Turn to the first three pages. Are you personally listed as the only Settlor/Grantor, the only current Trustee, and the only current Beneficiary? If yes, you have zero asset protection.

-

[ ] The Revocable Review: Does your document explicitly state that it is "Revocable at the discretion of the Grantor"? If those words are in your document, a creditor can force you to revoke it in court.

-

[ ] The Independent Barrier: Does your trust framework include an independent co-trustee, a successor trustee mechanism, or a "discretionary distribution" standard that legally prevents a judge from forcing a payout?

FROM THE INBOX

Q: "If I open an Irrevocable Asset Protection Trust to pass the control test, does that mean I can never sell my house or change the investments inside it?"

A: Absolutely not. This is the biggest misconception about irrevocable structures.

An "Irrevocable" trust simply means you cannot unilaterally wake up, destroy the trust, and take the property back into your personal, exposed name. However, the Trust itself is a living legal entity. As the manager (Trustee) of the trust, you retain the absolute power to manage the assets inside the vault.

If the Trust owns a piece of real estate, you can sell that house, pick up the cash proceeds inside the trust bank account, and use that cash to buy a completely different piece of real estate. The investments change, but the protective vault remains entirely intact. You keep the flexibility, the lawsuits keep their hands off.

HOW DID YOU LIKE THIS WEEK'S NEWSLETTER?

Your feedback helps us make this briefing even better.

If you found this intelligence valuable, please forward it to a friend or family member who needs to protect their legacy. We grow through your word-of-mouth.

Questions? Reply to this email or contact us at legalteam@lambergg.com

DISCLAIMER: This newsletter is for educational purposes only. Lambergg provides asset protection education, not legal advice. The information presented reflects general principles and may not apply to your specific situation. Tax laws, estate planning rules, and asset protection strategies vary by state and change frequently. Always consult with a qualified attorney and tax professional for advice tailored to your individual circumstances. Nothing in this briefing should be construed as creating an attorney-client relationship.

YOUR TURN

Did you realize that a standard Revocable Living Trust offers zero protection from lawsuits?

Are you realizing that your current estate planning documents might just be an "alter-ego" of your personal pocketbook? Reply directly to this email and let me know. I read every single response personally, and it helps me understand exactly what dangerous legal traps we need to expose next.

Until Friday, protect what matters.

The Lambergg Team