Welcome back to Lambergg’s Insiders.

If you are reading this, you probably log into your bank account, see the balance on your screen, and feel a sense of security. You assume that money sits in a vault, legally belonging to you, waiting for you to use it for your retirement or pass it down to your children.

Today, we are going to shatter that illusion.

We are going to expose a cold, hard legal truth that the banking industry desperately wants to keep hidden from the middle class. We are going to look at how federal banking laws actually view your money, and how the ultra-wealthy structure their assets to avoid being wiped out if the system falters.

Let's dive in.

LEGACY TIP OF THE WEEK

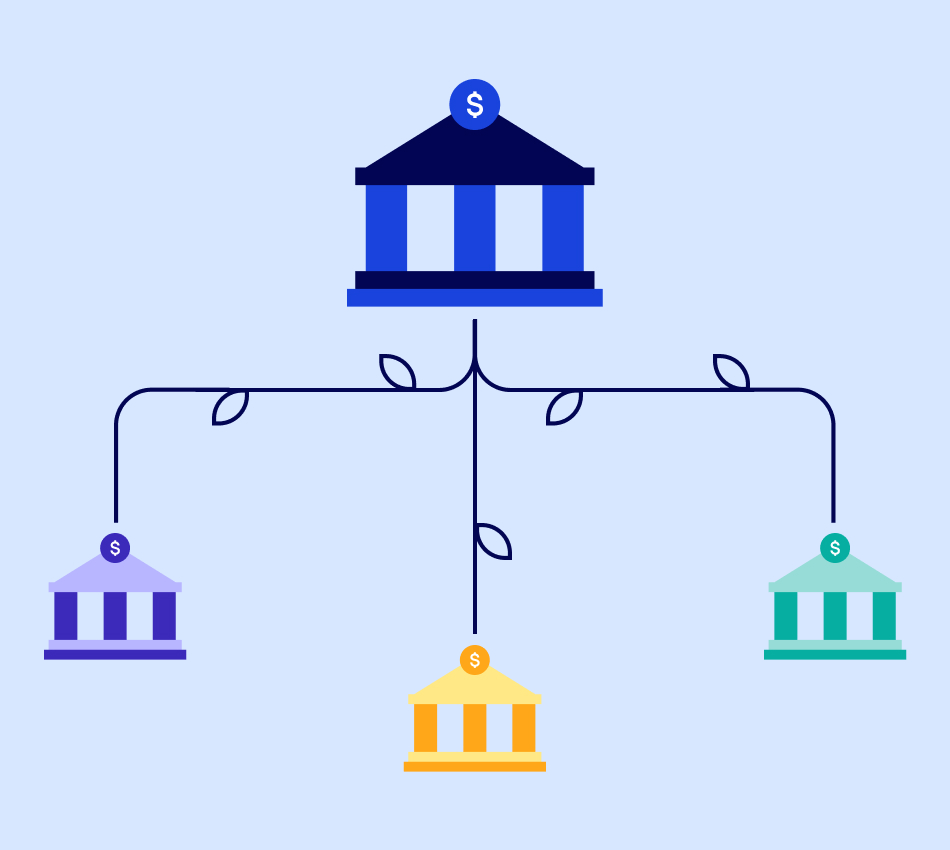

Sweep Network

If you recently sold a house or a business and deposited $800,000 into your personal checking account, you are in immediate danger. The FDIC only insures the first $250,000 of your deposits.

If your bank fails while you are holding $800,000 in a single account, $550,000 of your life's work is legally uninsured and completely exposed to the bank's creditors.

Never hold more than $250,000 in a single banking institution. If you need to keep large amounts of cash liquid, ask your bank about an "IntraFi" or "Sweep Network" account. This automatically spreads your large cash balance across multiple partner banks in the background, ensuring every single penny is covered by FDIC insurance without you having to manage a dozen different logins.

Why Your Deposit is Gone

When you hand your cash to a bank teller, you legally relinquish ownership of that money. You are no longer the owner; you are now legally classified as an "unsecured creditor" of the bank.

You essentially just gave the bank an unsecured loan. They can use your money to make risky investments, knowing they have the government as a safety net.

But what happens if the bank makes a mistake and faces total collapse?

In 2010, the government passed the 10,000-page Dodd-Frank Act. The public was told it was designed to stop taxpayer-funded bank "bailouts." But buried in the legalese, it created something far more dangerous for your personal wealth: The Bail-In.

Here is the mechanical breakdown of how a Bail-In legally seizes your money:

-

If a major bank is failing, the government places it into receivership.

-

Instead of using taxpayer money to save the bank, Dodd-Frank allows the bank to recapitalize itself by converting its debt into equity.

-

Because you (the depositor) are an "unsecured creditor," any money you have in the bank over the $250,000 FDIC limit can legally be seized and used to keep the bank's doors open.

The system was literally rewritten to protect the banking cartel by putting the financial burden directly on the backs of depositors.

You cannot put blind faith in a single financial institution. The ultra-wealthy do not leave their net worth sitting in cash as unsecured creditors. They utilize an Irrevocable Asset Protection Trust (like the Bulletproof Trust) to compartmentalize their wealth. They legally transfer their wealth into hard assets (like real estate and physical precious metals) and spread their remaining liquidity across multiple Trust-owned entities, remaining completely invisible and legally isolated from a systemic banking collapse.

CASE STUDY

The "Sentinel" Nightmare That Froze Millions

Sentinel Management Group was a cash-management firm that marketed itself to customers as a safe place to put their excess capital, promising solid returns and ready access to their cash.

Behind closed doors, Sentinel was secretly and fraudulently pledging hundreds of millions of dollars of its customers' supposedly safe assets to the Bank of New York Mellon as collateral for a massive overnight loan. When the economy faltered in 2007, Sentinel filed for Chapter 11 bankruptcy.

(A historic look at the 7th Circuit Court of Appeals)

Customers woke up to find their life savings completely frozen. The major bank stepped in and claimed it had a "senior secured" position over the customers' stolen money to cover its loan.

It took almost a decade of brutal, highly complex litigation in the 7th Circuit Court of Appeals just for the bankruptcy trustee to fight the bank and attempt to recover the misused customer funds. While the court ultimately ruled that the bank should have been suspicious of the fraudulent transfers, the damage to the families was already done. Years of their lives were spent fighting in court just to prove that their own money belonged to them.

When you leave your money exposed in the traditional system, you are at the absolute mercy of the people holding it.

The Exact Video Training Our Private Clients Use

If you want to ensure that your home, your business, and your cash stay exactly where they belong regardless of what happens with the global economy, you have to take the wheel.

The system wasn't built to protect you. It was built to move your money somewhere else.

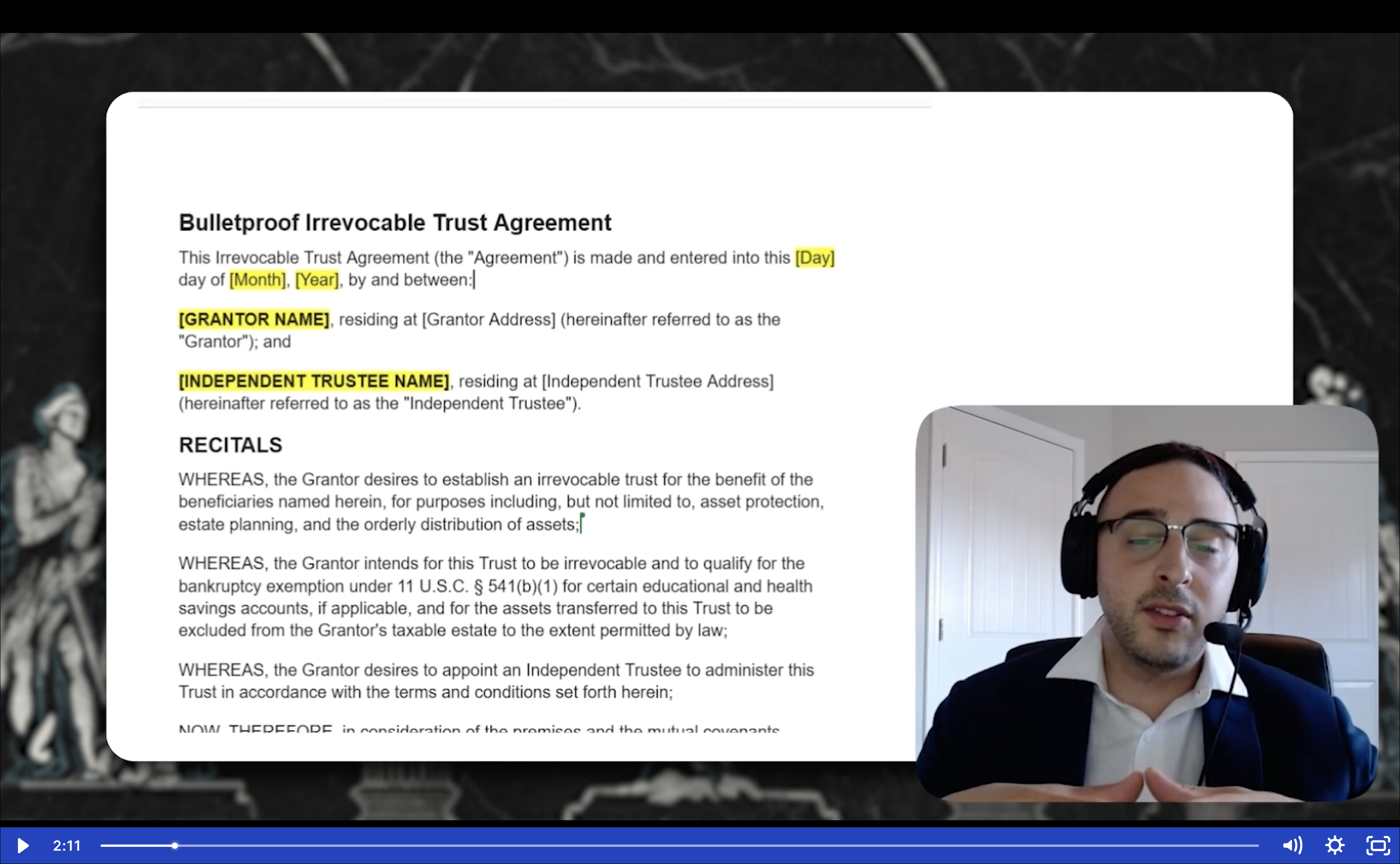

We took our complete Bulletproof Trust private client training, the exact step-by-step program we charge up to $20,000 to build for high-net-worth families and recorded the entire thing on video.

Inside the Bulletproof Trust Secrets video training, our lead trust attorney opens the legal documents and walks you through them page by page. Line by line. You will learn exactly how to structure every clause and fund every asset to shield your legacy from lawsuits, probate, divorce, and the IRS.

You hit play. You pause. You follow along. You build your own fortress.

You will know more about trusts than 95% of general-practice attorneys. You will be in control. Not your lawyer. Not the government. You.

→ Click Here to Access the Video Training ←

Liquidity Defense

Do not leave your life savings exposed to a banking collapse or a legal loophole. Take 10 minutes to audit your exposure today:

-

[ ] The Concentration Risk: Log into your primary banking app. Is your total balance over $250,000? If so, you have uninsured funds that are legally exposed to a Bail-In.

-

[ ] The "Hard Asset" Check: Are you 100% liquid? Asset protection requires diversification not just in stocks, but in asset classes. Consider moving a percentage of your exposed cash into tangible hard assets (real estate, metals) owned directly by your Trust.

-

[ ] The Entity Review: Do you hold your wealth in your personal name, or is it legally owned by a protective entity (like a Bulletproof Trust) that shields you from personal liability and public exposure?

FROM THE INBOX

Q: "If big banks are so dangerous, shouldn't I just move all my money into a small, local credit union?"

A: Moving to a local credit union is a great step for personalized service and avoiding massive Wall Street risk, but it does not solve the root legal problem. Even in a credit union (which is insured by the NCUA instead of the FDIC), your deposits still legally become the property of the institution. You are still an unsecured creditor. Furthermore, a local credit union does not protect your money from personal liabilities. If you cause a car accident, get divorced, or face a medical spend-down, a judge can freeze your credit union account just as easily as an account at Chase or Bank of America.

True security isn't just about changing where you bank; it is about changing how you legally own the money by utilizing an Asset Protection Trust.

HOW DID YOU LIKE THIS WEEK'S NEWSLETTER?

Your feedback helps us make this briefing even better.

If you found this intelligence valuable, please forward it to a friend or family member who needs to protect their legacy. We grow through your word-of-mouth.

Questions? Reply to this email or contact us at legalteam@lambergg.com

DISCLAIMER: This newsletter is for educational purposes only. Lambergg provides asset protection education, not legal advice. The information presented reflects general principles and may not apply to your specific situation. Tax laws, estate planning rules, and asset protection strategies vary by state and change frequently. Always consult with a qualified attorney and tax professional for advice tailored to your individual circumstances. Nothing in this briefing should be construed as creating an attorney-client relationship.

YOUR TURN

Did you realize that depositing money in a bank makes

you an "unsecured creditor"?

Have you ever worried about what would happen to your accounts if another 2008-style financial crisis hit? Reply directly to this email and let me know. I read every single response personally, and it helps me understand exactly what legal myths we need to shatter next.

Until Tuesday, protect what matters.

The Lambergg Team