Welcome back to Lambergg’s Insiders.

This past weekend, the business world was rocked by a massive, overnight collapse. A household name vanished in the blink of an eye.

Today, we are going to look at why this corporate disaster happened, and more importantly, what it exposes about the hidden, structural weaknesses in your own personal estate plan.

Let's dive in.

LEGACY TIP OF THE WEEK

Corporate Shield - Checkup

If you own an LLC or a Corporation for your small business or rental property, your state requires you to file an Annual Report or pay a franchise fee to remain in "Good Standing."

If you miss this simple filing (which is often due in the Spring), your state can administratively dissolve your LLC. The exact second your entity is dissolved, you lose your corporate shield. Any business liability or tenant slip-and-fall suddenly becomes your personal liability.

Go to your state's Secretary of State website this week. Search for your LLC's name and verify your status explicitly says "Active" or "In Good Standing." Do not let a $50 filing fee cost you your life savings.

Why No One is Invincible

On Saturday, May 2, 2026, Spirit Airlines abruptly ceased operations after 34 years in business. The announcement was sudden and severe. All flights were canceled immediately, leaving passengers stranded at airports and thousands of workers out of a job overnight.

The airline had been struggling under the weight of an $8.1 billion debt load following its second bankruptcy filing in August 2025. However, the final, fatal blow was an unforeseen storm: surging jet fuel costs driven by the war in Iran. When last-minute bailout negotiations for a $500 million federal rescue package collapsed over the weekend, the company had no choice but to begin an immediate, orderly wind-down of its operations.

Why are we talking about corporate bankruptcy in an asset protection briefing?

Because it exposes The Illusion of Invincibility.

You might look at your paid-off family home, your healthy 401(k), and your rental properties, and feel completely secure. You've worked for 30 or 40 years to build that foundation.

But if a 34-year-old corporation with billions of dollars in assets can be forced into total liquidation over a single weekend because of an unexpected storm, what happens when a storm hits your family?

The storms of life do not care about your history.

-

A medical crisis requiring $12,000 a month in long-term custodial care.

-

A catastrophic car accident where the judgment exceeds your insurance limits.

-

A frivolous lawsuit from a former employee or a disgruntled tenant.

If your assets are held in your personal name, or protected only by a fragile, standard Will, you are operating like an over-leveraged company. You are one crisis away from a judge or Medicaid forcing the "orderly wind-down" of your entire life's work.

The ultra-wealthy survive economic and personal storms because they build structural walls before the crisis hits. By legally transferring your home and your most valuable assets into an Irrevocable Asset Protection Trust (like the Bulletproof Trust), you separate the assets from your personal liability. If a storm hits you personally, the Trust remains untouched. You stop being a sitting duck and start operating like a fortress.

CASE STUDY

The "Orderly Wind-Down" of a 40-Year Legacy

David (68) built a highly successful HVAC company over four decades. He owned a $600,000 primary home and had $1.2 million in personal savings. He kept his business in an LLC, believing his personal assets were completely walled off from his professional life.

One of David's employees made a critical error during an installation, causing a severe electrical fire that destroyed a client's commercial building. The client’s insurance company sued David’s business for $3 million, far exceeding David's commercial liability coverage.

(Anonymized from a recent civil litigation review)

During the lawsuit, the opposing attorneys discovered that David occasionally used his business account to pay his personal property taxes, a classic case of "commingling funds." The judge pierced the corporate veil, completely invalidating the LLC's protection.

Because David's personal home and savings were held in his own name, they were instantly exposed. The court ordered the immediate seizure and liquidation of David's personal accounts and forced the sale of his family home to satisfy the judgment. Just like a bankrupt corporation, David’s 40-year legacy was forcibly wound down and erased.

If David had held his personal home and savings inside a Bulletproof Trust, the aggressive attorneys never could have touched them, regardless of what happened to his LLC.

The Exact Video Training Our Private Clients Use

If you want to ensure that your home, your business, and your cash stay exactly where they belong, with you and your children, you have to take the wheel.

The system wasn't built to protect you. It was built to move your money somewhere else.

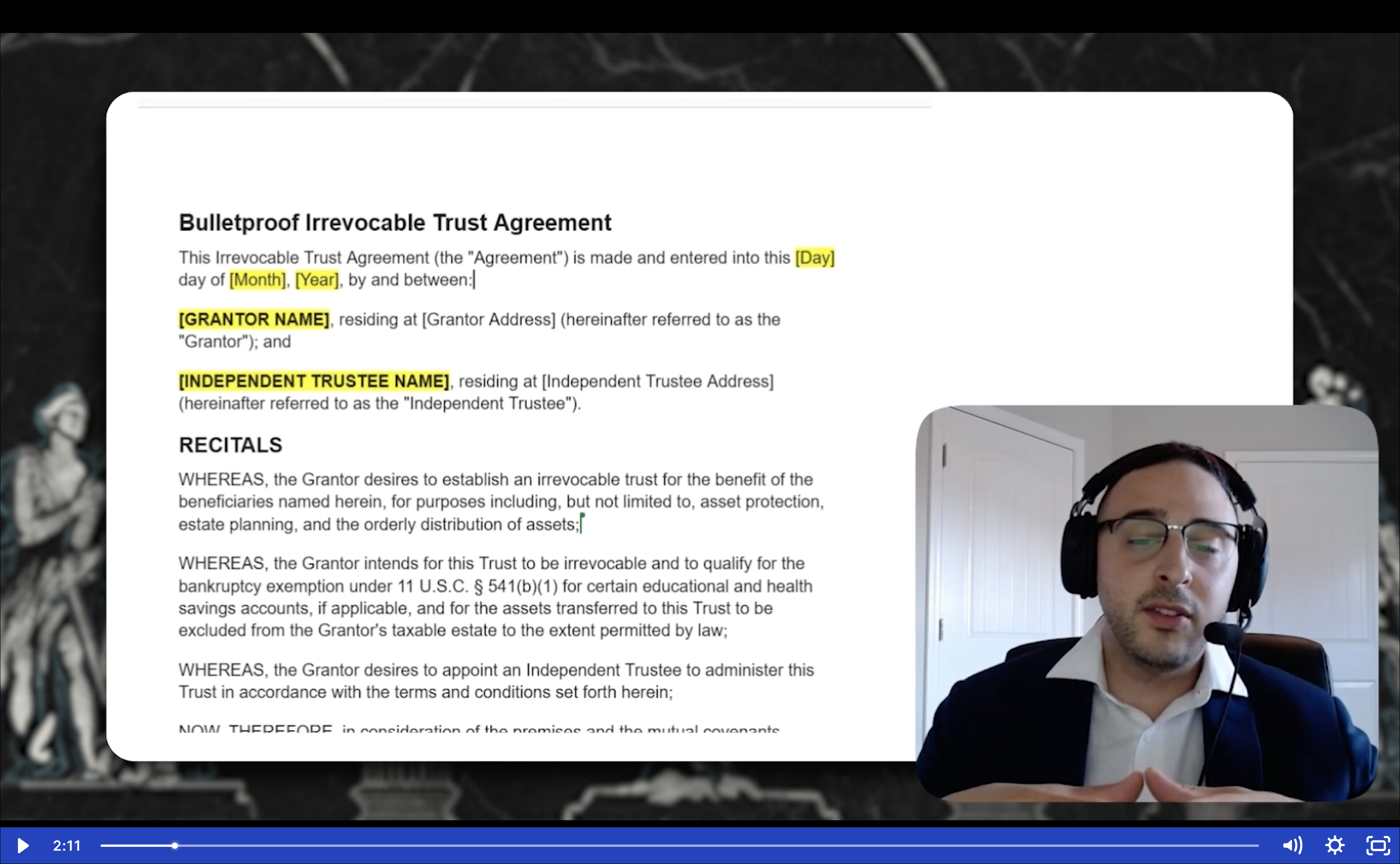

We took our complete Bulletproof Trust private client training, the exact step-by-step program we charge up to $20,000 to build for high-net-worth families, and recorded the entire thing on video.

Inside the Bulletproof Trust Secrets video training, our lead trust attorney Louis opens the legal documents and walks you through them page by page. Line by line. You will learn exactly how to structure every clause and fund every asset to shield your legacy from lawsuits, probate, divorce, and the IRS.

You hit play. You pause. You follow along. You build your own fortress.

(Make sure to subscribe to the channel while you are there. We are releasing high-level interviews like this every single week).

→ Click Here to Access the Video Training ←

The "Stress Test" Audit

Do not wait for a crisis to find out if your foundation has cracks. Take 10 minutes to audit your exposure today:

-

[ ] The "Naked Asset" Check: Look at your property deeds and major bank accounts. Are they listed in your personal name (e.g., "John Smith")? If yes, they are completely exposed to lawsuits and Medicaid liens.

-

[ ] The Commingling Check: Do you ever use your business or rental LLC debit card to buy personal groceries or coffee? Stop immediately. You are giving a judge the legal ammunition to pierce your corporate veil.

-

[ ] The "What If" Scenario: If you were sued for $2 Million tomorrow, what assets could you legally guarantee would survive the lawsuit? If your answer is "none," your plan needs an immediate upgrade.

FROM THE INBOX

Q: "If I get sued, can't I just quickly transfer my house into a Trust so the lawyers can't take it?"

A: No. This is a catastrophic mistake known as a "Fraudulent Conveyance."

If you are already facing a lawsuit, a creditor claim, or an impending Medicaid application, and you suddenly transfer your assets out of your name to hide them, the court will simply reverse the transfer. Worse, they can hold you in contempt or hit you with severe civil and criminal penalties.

Asset protection is a proactive shield, not a reactive bandage. You must build the vault before the robbery happens. The time to set up your Bulletproof Trust is right now, while the skies are clear.

HOW DID YOU LIKE THIS WEEK'S NEWSLETTER?

Your feedback helps us make this briefing even better.

If you found this intelligence valuable, please forward it to a friend or family member who needs to protect their legacy. We grow through your word-of-mouth.

Questions? Reply to this email or contact us at legalteam@lambergg.com

DISCLAIMER: This newsletter is for educational purposes only. Lambergg provides asset protection education, not legal advice. The information presented reflects general principles and may not apply to your specific situation. Tax laws, estate planning rules, and asset protection strategies vary by state and change frequently. Always consult with a qualified attorney and tax professional for advice tailored to your individual circumstances. Nothing in this briefing should be construed as creating an attorney-client relationship.

YOUR TURN

Does the sudden collapse of a 34-year-old company change how you view your own financial safety net?

Are you relying on "hoping nothing happens" as your primary asset protection strategy? Reply directly to this email and let me know. I read every single response personally, and it helps me understand exactly what blind spots we need to tackle next.

Until Friday, protect what matters.

The Lambergg Team