Welcome back to Lambergg’s Insiders.

We hope you had a restful Memorial Day weekend, honoring those who sacrificed for our freedoms and spending time with your loved ones.

As we get back to business this week, we are going to pull back the curtain on a massive realization. For decades, the middle class has been taught the ultimate American Dream: Work hard, pay off your house, put your name proudly on the deed, and build a massive savings account in your name.

But if you look at how billionaires and the ultra-wealthy actually structure their lives, they do the exact opposite.

Today, we are going to look at the foundational secret that legendary families use to protect their wealth, and show you exactly how you can legally apply the same strategy to your own life savings.

Let's dive in.

LEGACY TIP OF THE WEEK

Umbrella Insurance

Many homeowners buy a $1 Million or $2 Million Personal Umbrella Insurance policy, assuming it makes them invincible to lawsuits.

Insurance companies are in the business of collecting premiums, not paying claims. Umbrella policies are riddled with hidden exclusions. They often will not cover lawsuits involving business disputes, gross negligence, punitive damages, or incidents involving unlisted recreational vehicles (like a golf cart or boat). Worse, carrying a massive umbrella policy actually attracts aggressive plaintiff attorneys who see deep pockets to target.

Umbrella insurance is a good first line of defense, but it is not a vault. Never rely on an insurance adjuster to protect your life savings. True protection requires combining insurance with an impenetrable Trust structure, so if the policy fails or the lawsuit exceeds your coverage, your actual assets cannot be touched.

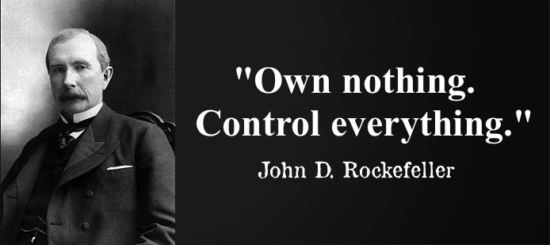

How to Control Your Wealth Like a Billionaire

John D. Rockefeller famously summarized the ultimate wealth protection strategy in one sentence:

"Own nothing, control everything."

The legal mechanics behind this quote are the reason generational wealth survives lawsuits, divorces, and the government.

Here is the difference between how traditional Americans hold wealth versus how the ultra-wealthy hold it:

Traditional Trap (The Sitting Duck): You own a $500,000 house. The deed is in your name. You have $400,000 in savings. The bank account is in your name. If you cause a severe car accident, a lawyer runs a public records search. They see your name attached to $900,000 in liquid equity. You are a massive, glowing target. When the judge rules against you, they take the house and the cash because you legally own them.

Billionaire Defense (The Ghost): The ultra-wealthy do not own their assets personally. They create legal entities specifically, Irrevocable Asset Protection Trusts. They transfer the house and the savings into the Trust. They write the rules of the Trust so that they are the "Manager" (Trustee) and they receive the benefit of the assets (Beneficiary). They still live in the house. They still spend the money. They control everything.

But legally? The Trust owns the assets.

If a billionaire gets sued personally, the lawyer runs a public records search. The billionaire's personal net worth shows up as $0. When the judge asks them to pay a massive settlement, the billionaire truthfully says, "I don't own anything." The Trust is a separate legal vault that the personal lawsuit cannot pierce.

You do not need a billion dollars to use this exact same legal mechanism. The laws that protect the Rockefellers and the Waltons are the exact same state and federal laws available to you. By upgrading from a basic Will to a Bulletproof Trust, you legally remove your name from the firing line while keeping absolute control over your lifestyle.

CASE STUDY

The Retirement Dream Wiped Out by a Teen Driver

Gary (67) recently sold his mid-sized landscaping business for $1.5 million. He deposited the cash into a high-yield savings account in his personal name. He also owned a home and a lake cabin. Gary felt incredibly proud of his net worth and thought his family was set for generations.

Gary let his 17-year-old grandson borrow his truck for the weekend. The grandson was texting and driving, ran a red light, and caused a catastrophic accident that permanently disabled a 35-year-old surgeon.

(Anonymized from a recent civil litigation review in Ohio)

Because Gary owned the truck, he was named in the "vicarious liability" lawsuit. The surgeon's legal team sued for $5 Million in lost future wages and medical care. Gary’s auto insurance maxed out at $250,000.

The aggressive lawyers ran a simple public search on Gary. They found the $1.5 million from the business sale and the deeds to both of his properties. The court seized the bank accounts and placed massive liens on both homes. Gary’s entire life's work was liquidated to pay the judgment.

If Gary had used the "Own Nothing, Control Everything" rule and placed the proceeds of his business sale and his real estate into an Asset Protection Trust, those assets would have been entirely invisible and legally unreachable by the victim's attorneys.

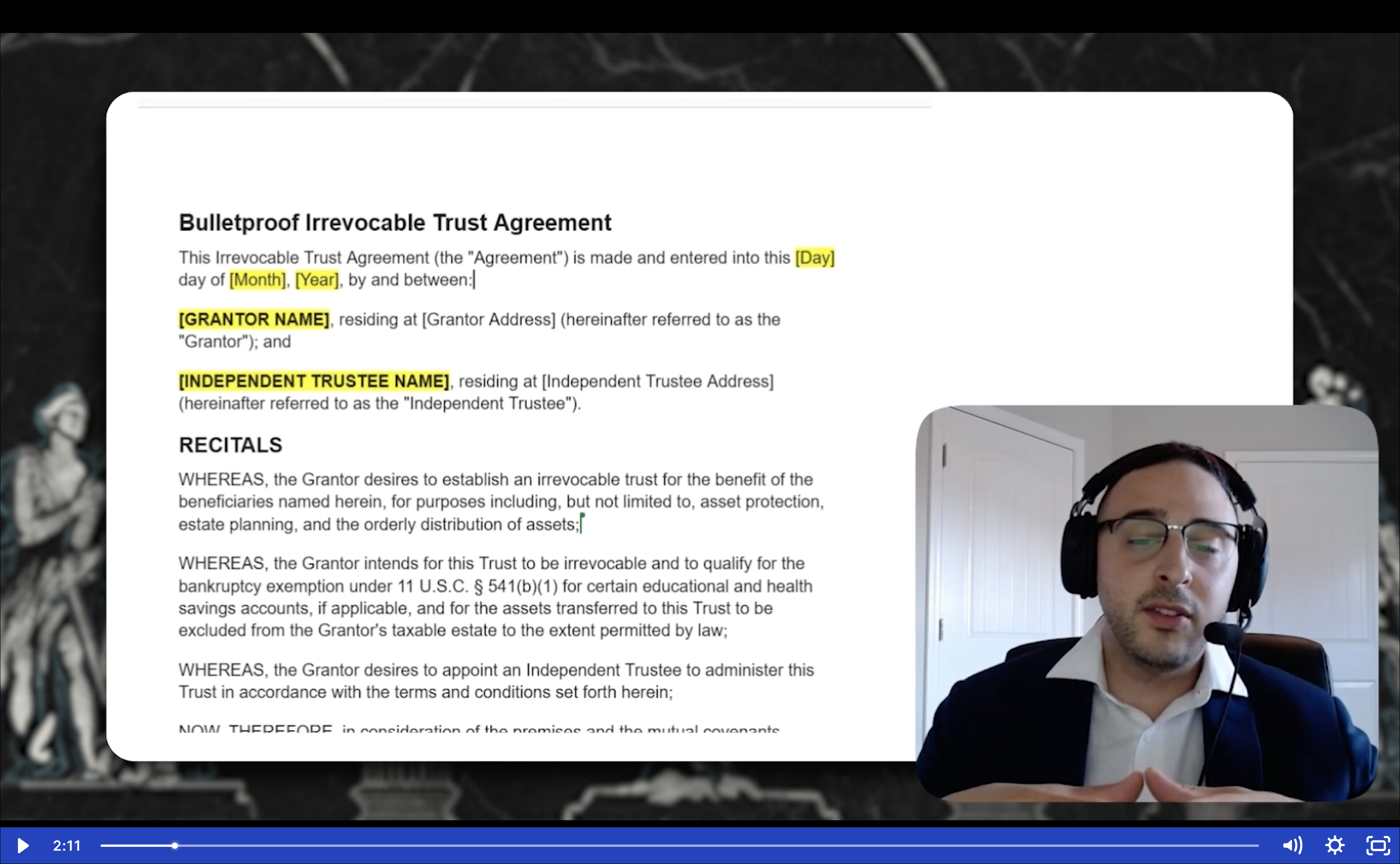

The Exact Video Training Our Private Clients Use

If you want to ensure that your home, your business, and your cash stay exactly where they belong regardless of what happens with the global economy, you have to take the wheel.

The system wasn't built to protect you. It was built to move your money somewhere else.

We took our complete Bulletproof Trust private client training, the exact step-by-step program we charge up to $20,000 to build for high-net-worth families and recorded the entire thing on video.

Inside the Bulletproof Trust Secrets video training, our lead trust attorney opens the legal documents and walks you through them page by page. Line by line. You will learn exactly how to structure every clause and fund every asset to shield your legacy from lawsuits, probate, divorce, and the IRS.

You hit play. You pause. You follow along. You build your own fortress.

You will know more about trusts than 95% of general-practice attorneys. You will be in control. Not your lawyer. Not the government. You.

→ Click Here to Access the Video Training ←

Billionaire Defense

Do not leave your hard-earned wealth exposed on the public record. Take 10 minutes to audit your visibility today:

-

[ ] The "Google" Test: Go to your county's property appraiser website (it is free public record). Type in your exact name. Does your primary home or rental property pop up? If yes, every hungry lawyer in your city knows exactly what you are worth.

-

[ ] The Revocable Illusion: If you have a Trust, check the title. If it says "Revocable Living Trust," you do not have asset protection. A Revocable Trust avoids probate, but it does absolutely nothing to stop a lawsuit or Medicaid. The court views a Revocable Trust as an extension of your personal pocket.

-

[ ] The Safe Asset Check: Are your most vulnerable assets (like teenage drivers or rental properties) legally walled off from your safest assets (like your primary home and retirement accounts)?

FROM THE INBOX

Q: "If I take my name off the deed and put my house into a Trust like the billionaires do, will I lose my property tax breaks and Homestead Exemption?"

A: No, not if it is drafted correctly. This is one of the biggest myths holding middle-class families back from protecting their homes.

When you use a properly drafted Asset Protection Trust, the Trust contains specific legal language that preserves your "Beneficial Interest" in the property. Because you retain the absolute right to live in the home, the vast majority of states allow you to keep your property tax freezes, senior discounts, and Homestead Exemptions exactly as they are today. You get the liability shield of a billionaire, without losing the tax benefits of a homeowner.

HOW DID YOU LIKE THIS WEEK'S NEWSLETTER?

Your feedback helps us make this briefing even better.

If you found this intelligence valuable, please forward it to a friend or family member who needs to protect their legacy. We grow through your word-of-mouth.

Questions? Reply to this email or contact us at legalteam@lambergg.com

DISCLAIMER: This newsletter is for educational purposes only. Lambergg provides asset protection education, not legal advice. The information presented reflects general principles and may not apply to your specific situation. Tax laws, estate planning rules, and asset protection strategies vary by state and change frequently. Always consult with a qualified attorney and tax professional for advice tailored to your individual circumstances. Nothing in this briefing should be construed as creating an attorney-client relationship.

YOUR TURN

Did you know that a basic "Revocable" Trust does absolutely nothing to protect you from a lawsuit?

Are you uncomfortable knowing that anyone with an internet connection can look up exactly how much your house is worth? Reply directly to this email and let me know. I read every single response personally, and it helps me understand exactly what legal myths we need to shatter next.

Until Friday, protect what matters.

The Lambergg Team