Welcome back to Lambergg’s Insiders.

If you have gone to the grocery store, paid a utility bill, or filled up your gas tank recently, you don't need the news to tell you what is happening. You feel it. You are paying significantly more money just to maintain the exact same standard of living you had a few years ago.

Many "financial gurus" will tell you to fight this by loading up on physical gold and silver, or by chasing 4% returns in high-yield savings accounts.

But today, we are going to look at the brutal mathematical and legal reality of those strategies. We are going to expose how inflation acts as a silent liquidation of your wealth, and why the traditional methods of fighting it actually expose your family to massive legal liability.

Let's dive in.

LEGACY TIP OF THE WEEK

Safe Deposit Box

People buying physical gold and silver often put it in a bank safe deposit box for security.

As we have covered before, safe deposit box rules are incredibly restrictive upon your death. But more importantly, the contents of a bank safe deposit box are completely uninsured by the FDIC. If the bank fails, is robbed, or if the government issues a systemic freeze, your physical metals are trapped or gone forever.

If you own physical precious metals, store them in a private, non-bank vaulting facility, or in a heavy-duty, high-security home safe. Most importantly, ensure the purchase receipt and the legal ownership of those metals is titled in the name of your Asset Protection Trust, not your personal name.

The Inflation Illusion and the "Hard Asset" Liability

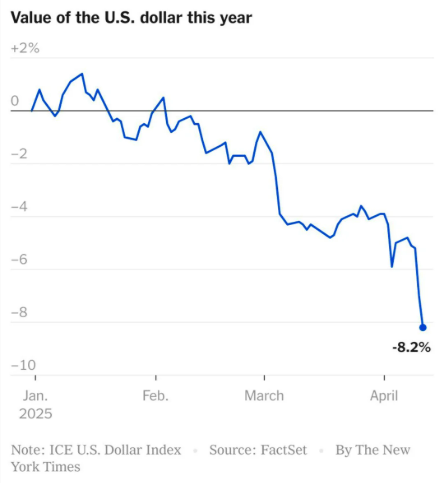

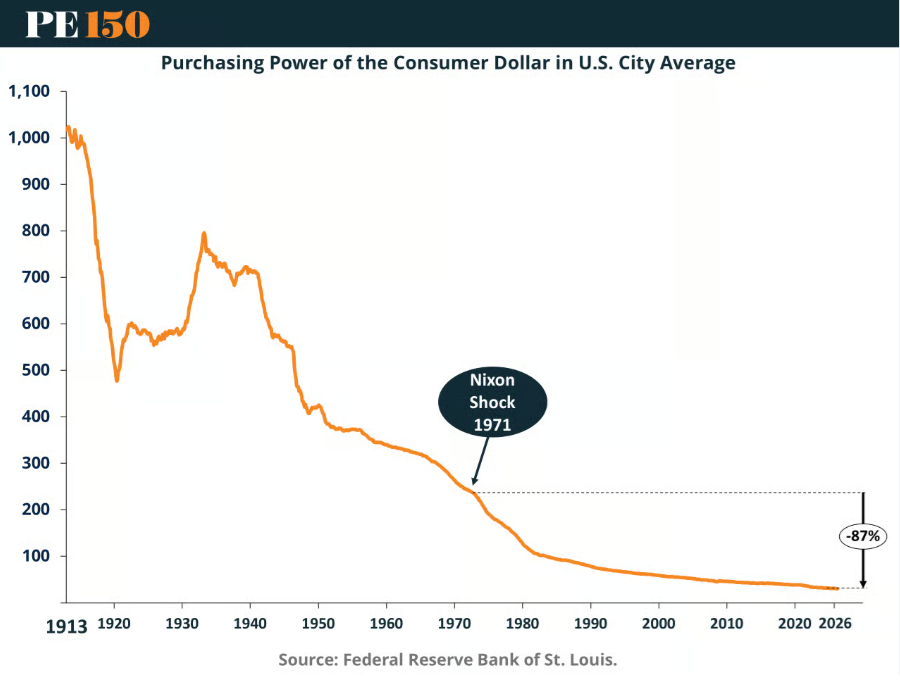

Let's look at the cold math. Since the Nixon Shock of 1971, the U.S. dollar has lost over 87% of its purchasing power. And the bleeding is accelerating. Between January and April of 2025 alone, the U.S. Dollar Index (DXY) plunged 8.2%.

The gap between the cost of living and everyday salaries is widening drastically. You aren't losing it, the gap is real, and it is silently liquidating your life savings.

When older Americans realize their cash is losing value, they typically make two panicked moves. Here is why both are legally dangerous if done incorrectly:

1. You move your cash into a high-yield CD or savings account paying 4%. But if the dollar is dropping by over 8% and real inflation is climbing, you are still losing money every day. Worse, by keeping massive amounts of liquid cash in the banking system in your personal name, you remain a highly visible "unsecured creditor" and a prime target for lawsuits.

2. You decide to convert your cash into tangible assets. With gold currently hovering around $4,200 an ounce, you buy physical bars and keep them in your home. It feels safe. But remember the fundamental rule: If you own it in your personal name, you can lose it.

If you cause a car accident, get sued, or face a massive Medicaid spend-down for nursing home care, those gold bars are legally considered personal, liquid assets. You will be forced to declare them under oath. If you try to hide them, you are committing perjury and bankruptcy fraud. The court will order you to hand your physical gold directly over to the plaintiff's attorney or the state.

The ultra-wealthy survive inflation by moving out of cash and into hard assets (real estate, precious metals, commodities) but they never hold those hard assets in their personal names.

They use an Irrevocable Asset Protection Trust. The Trust purchases the real estate. The Trust buys the gold. The Trust holds the investments. Because the Trust legally owns the inflation-hedged assets, the wealth is perfectly preserved against the declining dollar, while simultaneously being 100% shielded from lawsuits, creditors, and government seizure.

CASE STUDY

The "Off-the-Books" Silver Stash

Robert (71) didn't trust the banking system or the legal system. Over 10 years, he accumulated $150,000 worth of physical silver bars to protect his purchasing power, hiding them in a heavy floor safe under his workbench. He didn't tell his kids about it, assuming they would just find it when he passed away.

Robert suffered a severe stroke and required emergency, full-time memory care. His daughter, Linda, had to apply for Medicaid to cover the $11,000/month facility cost.

(Anonymized from a recent probate court review)

During the application process, the state auditor noticed large, unexplained cash withdrawals from Robert's bank account over the past decade. They demanded an explanation. Linda had no idea what the withdrawals were for. The state assumed Robert had given the money away fraudulently to hide it, and they denied his Medicaid application.

When Linda was forced to sell Robert's house to pay for his care, the new buyers found the floor safe, cracked it, and legally claimed the $150,000 in silver as part of the property purchase. Robert's entire inflation-hedge was lost because he operated in secret instead of using a legal, documented Trust structure.

The Exact Video Training Our Private Clients Use

If you want to ensure that your home, your business, and your cash stay exactly where they belong regardless of what happens with the global economy, you have to take the wheel.

The system wasn't built to protect you. It was built to move your money somewhere else.

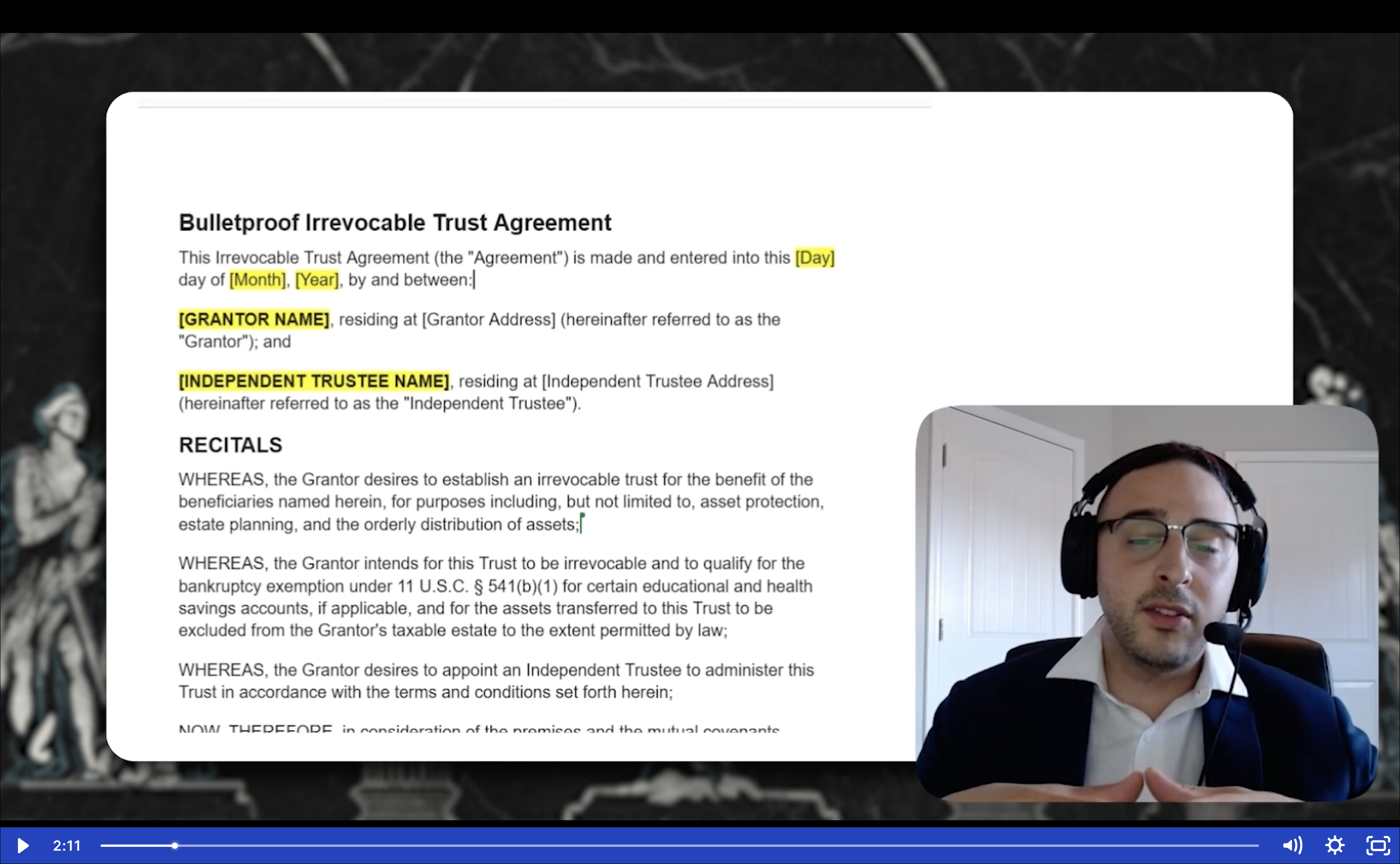

We took our complete Bulletproof Trust private client training, the exact step-by-step program we charge up to $20,000 to build for high-net-worth families and recorded the entire thing on video.

Inside the Bulletproof Trust Secrets video training, our lead trust attorney opens the legal documents and walks you through them page by page. Line by line. You will learn exactly how to structure every clause and fund every asset to shield your legacy from lawsuits, probate, divorce, and the IRS.

You hit play. You pause. You follow along. You build your own fortress.

You will know more about trusts than 95% of general-practice attorneys. You will be in control. Not your lawyer. Not the government. You.

→ Click Here to Access the Video Training ←

Purchasing Power

Do not let inflation and lawsuits attack your wealth from both sides. Take 5 minutes to audit your defense today:

-

[ ] Log into your bank accounts. If you are holding more than 6 months of living expenses in pure, uninvested cash, you are voluntarily paying an 8% "silent tax" on that money this year.

-

[ ] If you hold physical gold or silver, look at the invoice. Does it have your personal name on it? If yes, it is entirely exposed to your personal liabilities.

-

[ ] Real estate is one of the best inflation hedges on earth. But if the deed to your primary home or rental is in your personal name, you are carrying massive legal risk.

FROM THE INBOX

Q: "If I buy gold or silver coins with face values stamped on them, do I still have to pay capital gains tax when I sell them for a profit?"

A: Yes. Many internet promoters claim that because an American Silver Eagle has "One Dollar" stamped on it, it's legal tender and therefore tax-exempt when you sell it for $67 [1.1.3]. This is a dangerous myth.

The IRS classifies physical precious metals as "collectibles." If you hold them for more than a year and sell them for a profit, you are subject to a maximum long-term capital gains tax rate of 28%. Do not fall for sovereign citizen tax myths; structure your assets legally, pay the required taxes, and keep the IRS out of your life.

HOW DID YOU LIKE THIS WEEK'S NEWSLETTER?

Your feedback helps us make this briefing even better.

If you found this intelligence valuable, please forward it to a friend or family member who needs to protect their legacy. We grow through your word-of-mouth.

Questions? Reply to this email or contact us at legalteam@lambergg.com

DISCLAIMER: This newsletter is for educational purposes only. Lambergg provides asset protection education, not legal advice. The information presented reflects general principles and may not apply to your specific situation. Tax laws, estate planning rules, and asset protection strategies vary by state and change frequently. Always consult with a qualified attorney and tax professional for advice tailored to your individual circumstances. Nothing in this briefing should be construed as creating an attorney-client relationship.

YOUR TURN

Have you noticed the widening gap between the cost of living and the value of your savings?

Are you holding physical assets in your personal name without a structural shield? Reply directly to this email and let me know. I read every single response personally, and it helps me understand exactly what dangerous legal traps we need to expose next.

Until Friday, protect what matters.

The Lambergg Team