Welcome back to Lambergg’s Insiders.

If you are reading this, your primary home is likely your most valuable asset. It represents decades of mortgage payments, repairs, and family memories. You want to ensure it passes smoothly to your children without being drained by probate courts or nursing homes.

Because of this, millions of older Americans fall victim to the worst piece of "barbershop legal advice" in the country. A friend or a neighbor tells them: "Just go down to the county clerk and sign a Quitclaim deed selling the house to your kids for $1. It avoids probate and protects the house!"

Today, we are going to expose why this $1 piece of advice is a legal and financial time bomb.

Let's dive in.

LEGACY TIP OF THE WEEK

Out-of-State Executor

When you wrote your Will, you probably named your most responsible child as your Executor. But what if they live in another state?

Many states have incredibly strict, antiquated probate laws designed to keep money local. If your appointed Executor lives out-of-state, the probate judge may legally refuse to let them serve unless they can secure a massive "Surety Bond" (which can cost thousands of dollars out of pocket) or explicitly hire an in-state "Resident Agent" to oversee them.

Check your Will this weekend. If your named Executor lives out of state, you need to completely bypass the probate court system. By upgrading your Will to a Living Trust, your out-of-state child can step in as Successor Trustee immediately and manage your estate privately, entirely avoiding the court's geographical restrictions.

Why Giving Your Kids Your House Destroys Their Future

Filing a Quitclaim deed to put your adult child's name on your house seems incredibly simple. But the moment the county clerk stamps that paper, you trigger a cascade of legal disasters.

Here is the mechanical breakdown of why the "$1 House Transfer" destroys your wealth:

-

The exact second your child's name goes on the deed, your house legally becomes their asset. If your child gets into a severe car accident and is sued, the plaintiff's attorney will seize your house. If your child gets divorced, their ex-spouse can demand half the equity of your home in family court. If a judge orders the house sold to satisfy your child's debts, you can legally be evicted from the home you paid for.

-

If you transfer your house to your kids for $1, and then suffer a stroke three years later requiring nursing home care, Medicaid will audit you. Because of their strict 5-Year Lookback rule, they will view the $1 sale as a "fraudulent transfer." They will penalize you and completely refuse to pay your nursing home bills for years, bankrupting your family.

-

When you die and leave a house to your kids through a proper estate plan, they get a "Step-Up in Basis." This means the IRS values the house at the current market price, and your kids pay zero capital gains tax when they sell it. But if you give them the house while you are alive for $1, they inherit your original, decades-old purchase price. When they sell it, the IRS will hit them with a crushing capital gains tax bill, often stripping away 15% to 20% of the home's total equity.

You must separate the benefit of the house from the personal liability of your children.

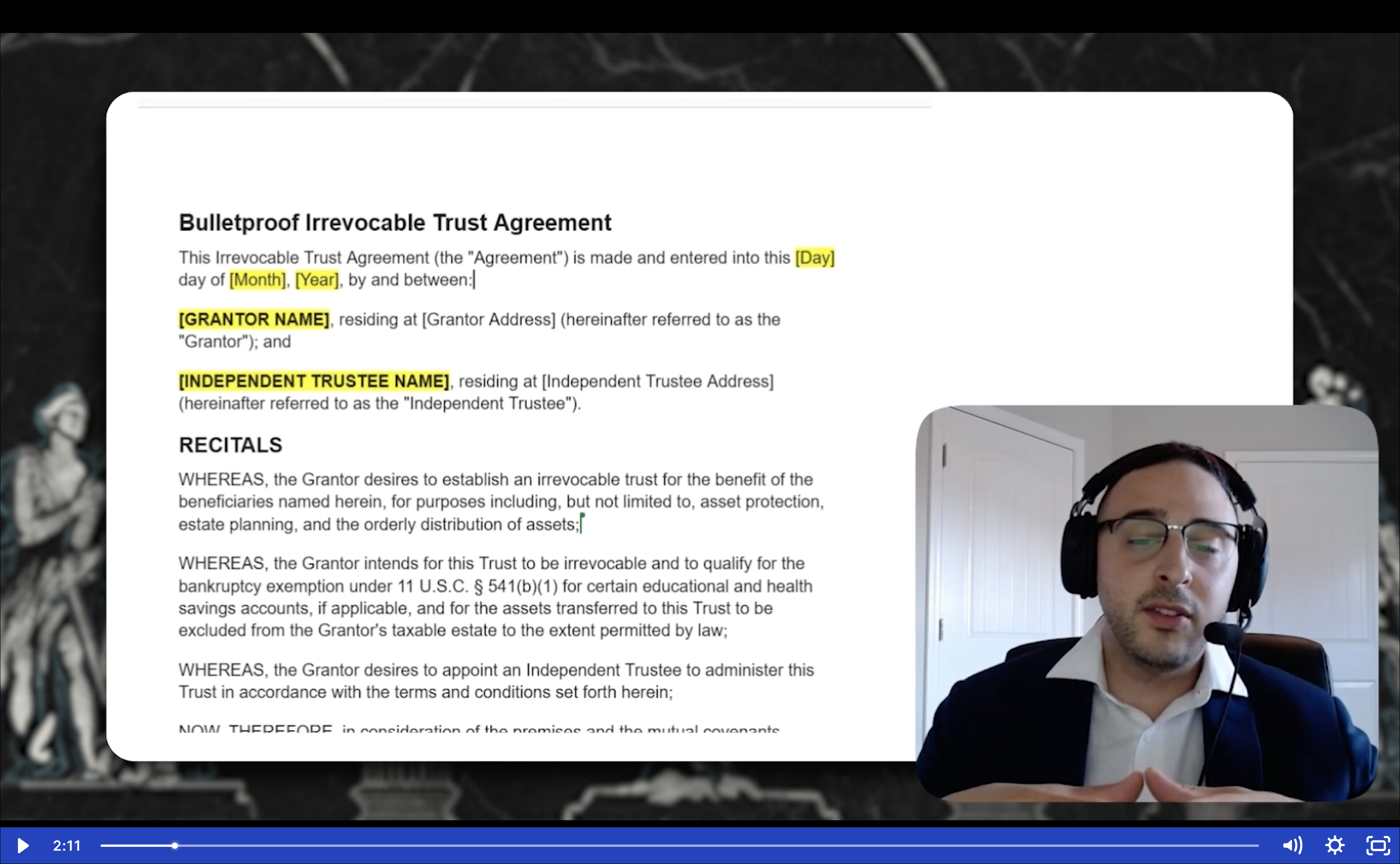

The wealthy never use Quitclaim deeds. Instead, they transfer their real estate into an Irrevocable Asset Protection Trust (like the Bulletproof Trust). The Trust owns the home. You retain the absolute right to live there for the rest of your life. Because your children do not personally own the house, their divorces, lawsuits, and bankruptcies cannot touch it. And because it is properly structured, it preserves the critical IRS tax loopholes and shields the equity from Medicaid.

CASE STUDY

The Bankruptcy That Left Mom Homeless

Eleanor (74) owned a modest $400,000 home, completely paid off. Wanting to make things "easy" for her only son, Mark, she went to an office supply store, bought a Quitclaim deed form, and transferred the house into Mark's name for $1. She continued to live in the house, pay the property taxes, and maintain the yard.

Four years later, Mark’s contracting business failed during an economic downturn. Drowning in corporate debt that he had personally guaranteed, Mark was forced to file for Chapter 7 bankruptcy.

(Anonymized from a recent federal bankruptcy court review)

Mark promised his mother her house was safe because she was the one living there. He was entirely wrong.

The federal bankruptcy trustee pulled Mark's public records and saw that he was the legal owner of Eleanor's $400,000 house. The trustee immediately seized the property as an asset of the bankruptcy estate. Eleanor went to court and pleaded with the judge, providing 30 years of mortgage receipts to prove it was truly her home.

The judge was sympathetic but stated the law was absolute: The name on the deed dictates ownership. The court forcibly sold Eleanor's home to pay off Mark's business creditors. Eleanor lost her 30-year sanctuary and was forced to move into a cramped rental apartment in her mid-70s, all because she tried to save a few dollars using a DIY property deed.

The Exact Video Training Our Private Clients Use

If you want to ensure that your home, your business, and your cash stay exactly where they belong regardless of what happens with the global economy, you have to take the wheel.

The system wasn't built to protect you. It was built to move your money somewhere else.

We took our complete Bulletproof Trust private client training, the exact step-by-step program we charge up to $20,000 to build for high-net-worth families and recorded the entire thing on video.

Inside the Bulletproof Trust Secrets video training, our lead trust attorney opens the legal documents and walks you through them page by page. Line by line. You will learn exactly how to structure every clause and fund every asset to shield your legacy from lawsuits, probate, divorce, and the IRS.

You hit play. You pause. You follow along. You build your own fortress.

You will know more about trusts than 95% of general-practice attorneys. You will be in control. Not your lawyer. Not the government. You.

→ Click Here to Access the Video Training ←

Deed Defense

Do not leave your sanctuary exposed to your children's hidden liabilities. Take 10 minutes to audit your property today:

-

[ ] The DIY Check: Did you ever file a Quitclaim deed adding your children to your home to "avoid probate"? If yes, your house is currently exposed to their creditors. You must consult an asset protection specialist to see if the transfer can be legally unwound.

-

[ ] The "Life Estate" Review: If you have a "Life Estate" deed, realize that while it protects your right to live there, the "remainder interest" is still a target for your children's lawsuits.

-

[ ] The "Trust Verification": Pull your property deed online. The "Grantee" line should not list you or your children personally. It should explicitly list the name of your Trust (e.g., The Smith Family Asset Protection Trust).

FROM THE INBOX

Q: "I am perfectly healthy right now. Can't I just wait to put my house into an Asset Protection Trust until I actually get sick or need a nursing home?"

A: This is the most dangerous form of procrastination in estate planning.

Medicaid utilizes a strict 5-Year Lookback Period. If you wait until you get a bad diagnosis to transfer your house into an Irrevocable Trust, Medicaid will audit the transfer, flag it, and issue a massive penalty period. They will legally refuse to pay for your care for years based on the value of the home you transferred.

To successfully protect your home from long-term care costs, the house must be safely inside the Trust for a full 60 months before you apply for assistance. Asset protection is a proactive shield, not a reactive bandage. You must dig the well before you are thirsty.

HOW DID YOU LIKE THIS WEEK'S NEWSLETTER?

Your feedback helps us make this briefing even better.

If you found this intelligence valuable, please forward it to a friend or family member who needs to protect their legacy. We grow through your word-of-mouth.

Questions? Reply to this email or contact us at legalteam@lambergg.com

DISCLAIMER: This newsletter is for educational purposes only. Lambergg provides asset protection education, not legal advice. The information presented reflects general principles and may not apply to your specific situation. Tax laws, estate planning rules, and asset protection strategies vary by state and change frequently. Always consult with a qualified attorney and tax professional for advice tailored to your individual circumstances. Nothing in this briefing should be construed as creating an attorney-client relationship.

YOUR TURN

Have you or any of your friends ever considered "selling" a house for $1 to avoid probate?

Are you worried about how your child's financial situation or marriage could eventually impact the inheritance you leave them? Reply directly to this email and let me know. I read every single response personally, and it helps me understand exactly what blind spots we need to tackle next.

Until Tuesday, protect what matters.

The Lambergg Team