Section 1: THE RED ALERT

The $15 Million Estate Tax Exemption Is Now Permanent. Here's What It Means for Your Family.

The What Happened:

Congress passed the "One Big Beautiful Bill Act" this year(2025), and it fundamentally changes the estate tax landscape. Starting January 1, 2026, the federal estate and gift tax exemption rises to $15 million per person (or $30 million for married couples). More importantly: the dreaded "sunset" provision is gone.

For the past two years, estate planners have been warning clients about the 2025 sunset, the moment when exemptions were set to plunge from roughly $14 million back down to about $7 million per person. That would have meant millions of Americans suddenly facing 40% estate taxes on wealth they'd assumed was protected.

That cliff is now gone. The new $15 million exemption is indexed for inflation and unless a future Congress changes it, it's here to stay.

Why This Matters for Your Wallet:

Let's be direct: If your estate is under $15 million (or $30 million jointly), you likely won't owe federal estate taxes. That's the good news.

But here's what most people miss: state estate taxes still exist, and they operate on completely different rules.

For example, New York's estate tax exemption in 2025 is just $7.16 million, less than half the federal limit. Worse, NY has a "cliff tax": if your estate exceeds the exemption by more than 5%, you lose the exemption entirely. And New York doesn't allow portability between spouses like the federal system does.

Translation: A married couple in New York with a $15 million estate could owe zero federal estate tax but hundreds of thousands in state taxes, unless they plan correctly.

Lambergg Interpretation:

Most lawyers will tell you: "Great news! The exemption went up. You can relax."

The reality is more nuanced: Higher exemptions solve one problem (federal estate tax) while leaving others completely unaddressed.

Consider: The new law does nothing to protect your assets from lawsuits, creditors, Medicaid recovery, or divorce courts. A $15 million exemption means nothing if a judgment creditor can seize your home tomorrow.

This is why an arm's-length Irrevocable Trust (what we call the Bulletproof Trust) remains superior to a standard Living Trust—even in this new environment. The Bulletproof Trust isn't just about avoiding estate taxes. It's built on 11 U.S.C. § 541(c)(1), federal bankruptcy law, which provides protection that state-based asset protection trusts simply can't match.

The wealthy have always understood this: Tax planning and asset protection are two different disciplines. You need both. The One Big Beautiful Bill Act helps with taxes. Your trust structure handles everything else.

Section 2: FROM THE FIELD

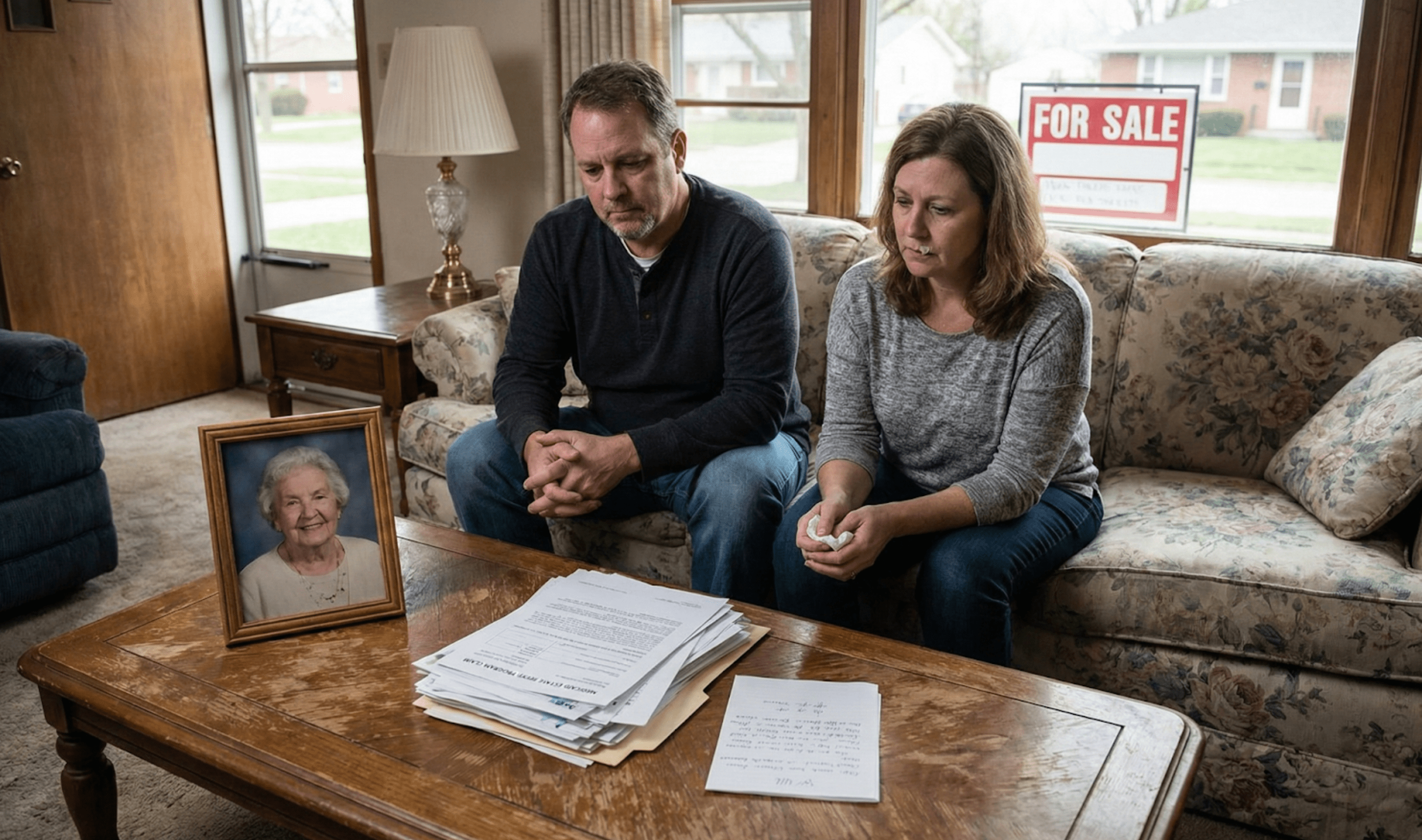

"My Mother Paid $180,000 for Nursing Home Care. After She Died, Medicaid Took the House Anyway."

We saw a discussion this week in an estate planning community that broke our hearts and reinforced why we do this work.

The Story:

A woman in Ohio shared that her mother spent four years in a nursing home, with Medicaid covering a significant portion of the costs after her savings ran dry. The mother had a will that left the family home to her three children. She assumed that since Medicaid was "paying" for her care, the house would pass to her kids.

She was wrong.

Six months after her mother passed, the family received a letter from the state's Medicaid Estate Recovery Program (MERP). The letter stated that Medicaid intended to file a claim against the estate for $287,000, the total amount Medicaid had paid for nursing home care. The family home, valued at approximately $210,000, was the only significant asset remaining.

The children were forced to sell the house to satisfy the MERP claim. After legal fees and closing costs, they received nothing.

The Lesson:

This family made a common mistake: They relied on a Will to protect the home.

Here's what most people don't understand: A Will only controls what happens to your assets after you die. It does nothing to protect those assets from creditors including the government.

All 50 states are required by federal law (OBRA 1993) to operate Medicaid Estate Recovery Programs. If you receive Medicaid-funded long-term care after age 55, the state must attempt to recover those costs from your estate after death. Your home is often the primary target because it's usually the last asset of significant value.

The home is "exempt" while you're alive, meaning it doesn't count against Medicaid's asset limit when you apply. But exempt doesn't mean protected forever. It simply means Medicaid waits until you die to collect.

The Fix:

Had the mother transferred her home into a properly structured Irrevocable Trust (like a Medicaid Asset Protection Trust or the Bulletproof Trust) at least five years before applying for Medicaid, the home would not have been part of her estate. The state's MERP claim would have found... nothing to recover.

The five-year period matters because of Medicaid's "Look-Back Rule." Any assets transferred within 60 months of your Medicaid application can trigger a penalty period of ineligibility. But transfers made before that window? They're beyond Medicaid's reach.

The key insight: Once assets are properly transferred to an irrevocable trust, you don't legally "own" them anymore. They're held for your benefit, but they're not yours. And creditors including Medicaid can only collect from what you own.

This is exactly the mechanism that the Bulletproof Trust leverages. Control the steering wheel, not the title.

Section 3: THE PROTECTION TOOLKIT

This Week's Actionable Tip: Check Your Beneficiary Designations (They Override Your Will)

Here's a non-obvious truth that catches families off guard every single week:

Beneficiary designations on life insurance, retirement accounts (401k, IRA), and "payable on death" bank accounts override your Will entirely.

Your Will might say: "I leave everything to my three children equally." But if your $500,000 life insurance policy still lists your ex-spouse from 1987 as the beneficiary? That ex-spouse gets the money. Your children get nothing from that policy. And there's almost nothing anyone can do about it.

Your action item for this week: Pull out every account that has a beneficiary designation, life insurance, annuities, 401(k), IRA, bank accounts with POD/TOD designations and verify that the named beneficiaries are exactly who you intend them to be. Update any that are outdated.

This takes 30 minutes. It could save your family from years of heartache and legal battles.

Pro tip: If you have an irrevocable trust, consider naming the trust as beneficiary (where appropriate) rather than individuals directly. This can add an extra layer of protection and ensure distributions happen according to your trust's terms, not subject to a beneficiary's creditors, divorce, or poor financial decisions.

If you found this briefing valuable, please forward it to a friend or family member who needs to protect their legacy. We rely on your word-of-mouth, not ads.

Questions? Reply to this email or contact us at legalteam@lambergg.com

DISCLAIMER: This newsletter is for educational purposes only. Lambergg provides asset protection education, not legal advice. The information presented reflects general principles and may not apply to your specific situation. Tax laws, estate planning rules, and asset protection strategies vary by state and change frequently. Always consult with a qualified attorney and tax professional for advice tailored to your individual circumstances. Nothing in this briefing should be construed as creating an attorney-client relationship.

Until next week, protect what matters.

The Lambergg Team